We’re in a truly unprecedented situation. It’s not the first pandemic mankind has been faced with, but it’s by far the most acute one in modern history. In addition to the health crisis, the pandemic also brings an economic and social crisis — and if we’re being perfectly honest, no one really knows how this will all shape the future. But perhaps, past events can give us a few lessons for what can work and what doesn’t.

Trickle-down fuels inequality, oil is vulnerable, and “safe” industries aren’t safe

In the post-WWII period, life gradually improved in many parts of the world. For Americans, the period from the late 1940s to the 1970s was a booming economic period.

But the boom didn’t last forever.

The 1970s were rattled by not one but two oil crises. Economic growth started wavering, and people were faced with the reality that accelerated growth isn’t always sustainable. Some traditional industries, even ones once thought to be rock-solid, went into decline. Many never recovered.

The US government reacted, and the most notable shift was brought in by Ronald Reagan. Reagan implemented a series of reforms that would put the US on a decisive course for decades to come.

Reagan pushed for deregulation, getting rid of state-owned companies and moving to cut back taxes for higher incomes. This decision was based on the belief that the money would be reinvested and then “trickle down” to everybody.

The effects of this trickle-down economy are widely felt to this day: on one hand, the practice was successful in creating a culture of entrepreneurship and overall, the country’s GDP continued to grow, but unemployment and inflation also steadily grew.

Here’s a problem: much of that growth went into the pockets of the few. In fact, if you look at the poorest group, their cumulative incomes have actually decreased compared to the 1980s — which is crazy considering how much the richest group’s earnings increased.

There are many ways to look at how the trickle-down economy fuels inequality, but here’s a very simple and clear graph, illustrated by Mirko Lorenz, co-founder of Datawrapper: people’s productivity continued to increase, but their income remained stable.

There are of course other factors at play here, such as automation. But automation and industry changes alone cannot explain this — especially as the trend was not nearly as extreme in other countries.

Even before the pandemic, the current US administration had granted tax cuts for the country’s richest, so the trend is expected to exacerbate. If we’re looking at relief programs that will only help the top of the economic pyramid in the hope of it trickling down, we can expect rising inequality.

As for industries traditionally considered stable and reliable, we’ve already seen that this is not nearly a guarantee. For the first time in history, oil prices turned negative, and the economic forecasts project that this is only the first in a number of shakeouts that the oil industry will face. The rise of renewables is also expected to accelerate the decline of oil companies, though this is far from a guarantee. Another mainstay industry that has been heavily affected by the pandemic is the meat industry, where thousands of infections have been detected.

With the distancing measures likely to remain active in the future, it’s hard to say which industries will suffer the most and which will require the most support.

More workers, more debt

When wages stagnate (which has happened following Reaganomics and is likely to happen in the following years), more women go into the workforce — especially mothers. That’s good on one hand because it favors equality and independence, but on the other hand, the US is the only OECD country without a national statutory paid maternity, and many of the working mothers have small children without anyone to care for them.

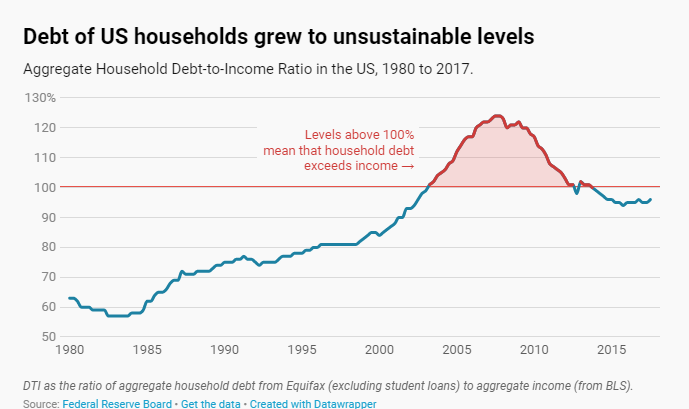

Another issue to consider is that despite more people going into the workforce, household debt has increased dramatically. Ironically, it was the 2008 crisis that ultimately brought the debt levels to sustainable levels.

Lessons from the Spanish Flu: You save the economy by saving lives

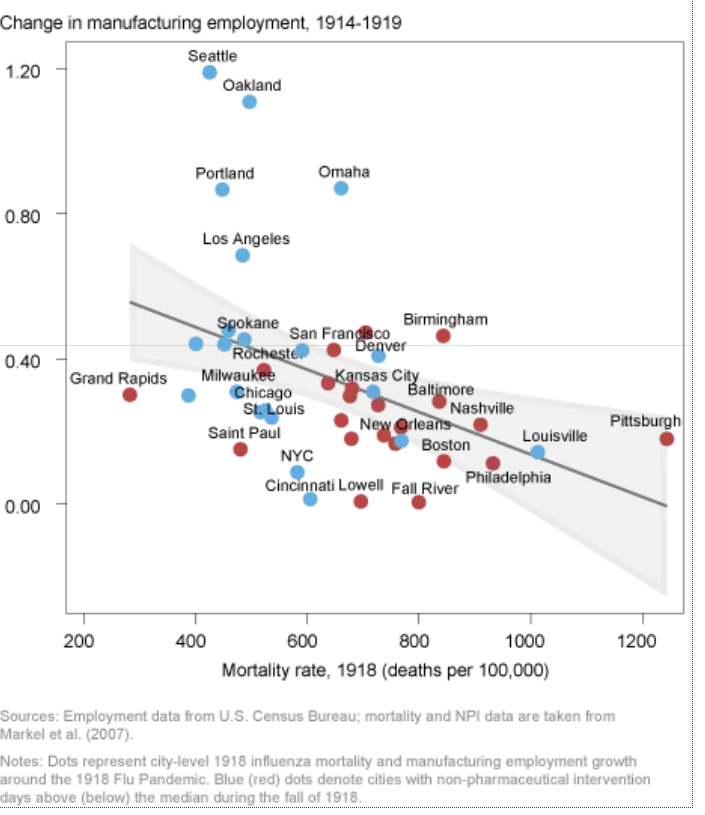

There is only one event in recent history that carries a resemblance to the current situation: the Spanish Flu pandemic.

A recently-published study analyzed the economic effect of the Spanish Flu on American cities. The researchers found that it was the pandemic itself that caused the economic damage, and the public health measures, while disruptive, had a net positive impact by saving lives. In other words, the benefits these measures provide by saving lives is greater than the damage done through disruption.

“Altogether, our evidence implies that it’s the pandemic and the associated spike in mortality that constitute the shock to the economy,” the authors write.

The bottom line

Few things are certain in the coming period, but one of the certainties is that the global economy will be subjected to massive stress — and this stress is very likely to exacerbate what is an already very pressing inequality, both in the US and outside of it. We are already seeing major macroeconomic areas coming up with stimulus plans, and these plans could set a direction for decades to come.

It’s very easy for these plans to chase economic growth and leave behind certain groups, specifically disadvantaged groups. It’s not difficult to envision a post-pandemic world with economic inequality on steroids.

Much of the world is already struggling with inequality — and extreme inequality has been shown to increase health and social problems, crime rate, and increasing political instability.

In our understandable hurry to restart the economy, we must not forget that saving lives is also saving the economy, and leaving people behind can create even more trouble down the line.

{kind=link}