- 💡 Lived experiences, like hyperinflation, significantly ‘rewire’ the brain, affecting financial decisions in the future and possibly across entire generations.

- 🧠 Behavioral economics shows people make financial decisions based on habits, instincts, and psychological biases, not solely rational thinking.

- 📉 Bridging economics with neuroscience, researchers show how the experience of high inflation strongly influences future homeownership and investment decisions — even in times of low inflation and in totally different economic environments.

Economics has traditionally viewed individuals as rational optimizers, perfectly processing information to make the best decisions within their constraints like the obeying automatons that they are. It took economists a while before they realized that’s not at all how people make financial decisions, which is how behavioral economics came to be.

Behavioral economics combines ideas from psychology and economics to understand how people actually make decisions, rather than how they should make decisions according to traditional economic theories. Rather than rational agents, most people are creatures of habit and instinct who make decisions based on gut feeling and psychological biases. Yet, even this progressive field often still treats humans as fundamentally computer-like in their information processing, not capturing the full scope of the complexity of human economic decision-making.

Ulrike Malmendier, professor of finance and economics at the University of California, Berkeley, argues through her multi-decade research that lived experiences have a profound experience on all economic behavior.

Her research, for instance, shows that significant social and economic events, such as hyperinflation, can literally rewire the brain, leading to long-lasting effects on financial decision-making. This reprogramming persists even after the economic climate stabilizes, influencing people’s responses to similar situations in the future.

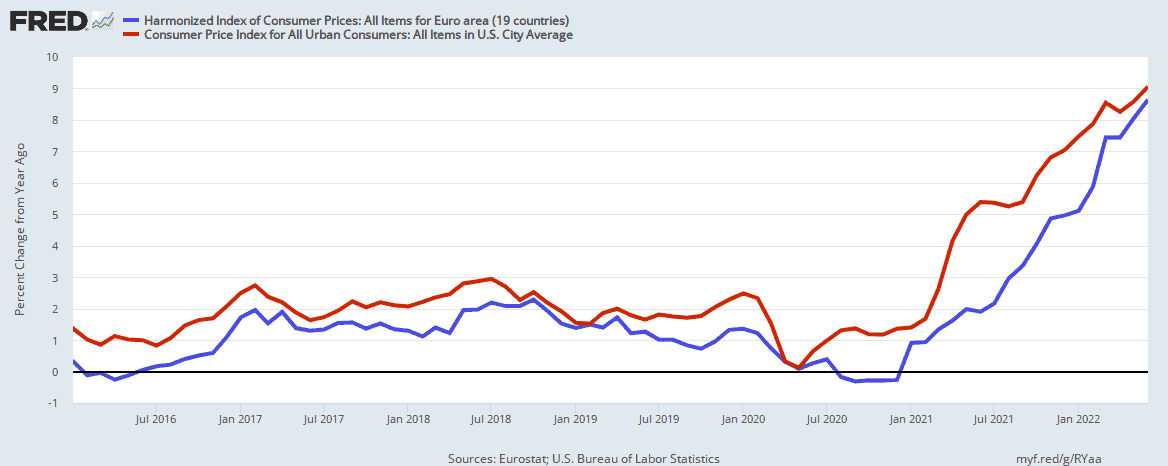

The experience and expectation of inflation

The last few years since the pandemic have been rough for everyone. Besides the tragic loss of life and human suffering owed to a pandemic unprecedented in the last century, the events that unfolded since 2020 have sent rippling shockwaves into the global economy. As if the supply chain shocks and subsequent money printing weren’t concerning enough, then came Russia’s invasion of Ukraine which caused energy prices to surge — and with them, the price for virtually everything else.

The result has been very high inflation whose effects on the economy could linger on for many years to come — even after inflation is brought back under control. That’s because not only do prices surge during a high-inflation environment, but also people’s fears, anxiety, and concerns.

Young people of Gen Z, who have never gone through something like unlike their parents and grandparents, are particularly vulnerable. They may have become permanently scarred and afraid prices will continue to rise, which could affect their financial decisions for the rest of their lives.

In other words, there’s a big difference between the hard, cold numbers and graphs that central banks show and how people perceive inflation in their daily lives. When Fed chair Gerome Powell goes on TV talking about “soft landings” and how inflation is “cooling”, a single mom doing grocery shopping might come to a different conclusion. Ultimately, this subjective experience impacts inflation expectations, extremely complicating the dynamics at play and throwing a wrench into economists’ fancy mathematical models.

“What this new research about the effects of experience says is that if I live through a crisis — for example, a high inflation crisis — that changes me. That triggers something in me, some fears. If I see prices and taxes that keep increasing, and I’ve lived through that for a while, it rewires my brain. It literally does. Actually, neuroscience tells us this. And we need to take that into account in economics,” Malmendier told ZME Science during an interview at the Falling Walls conference in Berlin.

“There’s this view that once we are out of this inflation period and inflation is back at 2%, everything will be back to normal. To assume that all the people in the country will act as before is just wrong because we have been rewired. We have been affected.”

The trauma of inflation — and its rippling effects

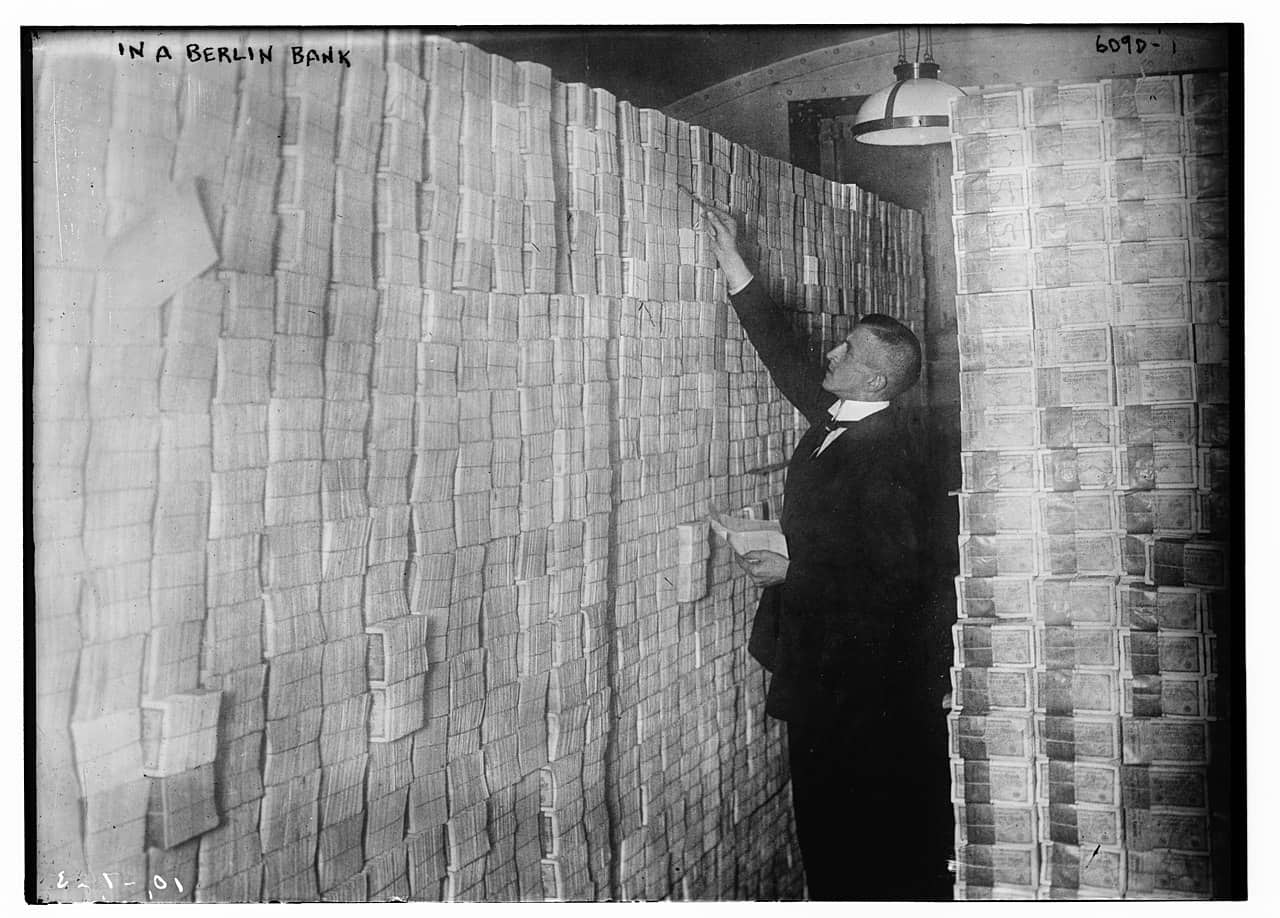

Like all Germans, Malmendier grew up with the specter of inflation and what it can do to people’s livelihoods. In 1923, the Weimar Republic economy collapsed, triggering a catastrophic spiral of hyperinflation. In January 1923, a US dollar cost 17,000 marks. In December, the exchange rate topped out at 4.2 trillion marks to the dollar — a staggering 2.5 billion percent increase.

The rapid devaluation of Germany’s currency created some ludicrous sights. The value of paper money evaporated so quickly that some companies paid employees in the late morning so they could rush off and spend their wages at lunchtime. It was common to see shoppers hauling buckets, bags, and even wheelbarrows full of banknotes to pay for groceries or simple items. In some situations, people didn’t bother to count money anymore — weighing it was much more effective.

Banknotes from last month were used by children as toys like Monopoly money, while their parents used their Papiermark (the currency of the Weimar Republic) to light the fire. Millions of people found themselves bankrupt and struggling to make ends as their paper money was worth less than toilet paper. The middle class was completely obliterated. For many, it was simply futile to carry money anymore, so they turned to bartering.

Amid this chaos, Germans struggled to understand what was happening to their country and why. They naturally doubted the ability of the state to keep things under control, which set the stage for Adolf Hitler’s takeover in 1933 — and we all know what followed next.

The German people who lived through these traumatic events were scarred for life, permanently altering their relationship with money and finance in general. But remarkably, traditional economics hasn’t considered these important long-lasting effects.

The long-lasting memory of inflation

Whenever inflation rises beyond the norm — which is anything above the “healthy” inflation rate of 2% per year — central banks roll up their sleeves and start pressing levers to tone it down. Typically, they tinker with the interest rate and the money supply. The expectation is that once this delicate balancing act is successful and inflation is back under 2%, consumer behavior will be back to normal.

“The problem is it doesn’t work,” says Malmendier.

Inspired by the Weimar hyperinflation and its behavior-altering effects, Malmendier studied other historical high inflation events, from America’s double-digit inflation from the 1970s and 1980s to the more recent hyperinflation streak in Argentina. This research revealed a global pattern that showed living through inflation can dramatically change the way decide to spend, save, and borrow money, irrespective of the country.

“Over and over, you see, independent of the country or the decade you look at, that people whose lives have been characterized by a lot of high inflation, they continue to live with that fear, even when the inflation is not there.”

In a 2023 study published in the Journal of Finance, Malmendier and Alexandra Steiny Wellsjo from the University of California San Diego investigated how past exposure to high inflation impacts home ownership. Investment in buying a home and real estate, in general, is strongly motivated by protecting one’s wealth from currency devaluation.

The researchers found a strong correlation between past high inflation rates and higher homeownership. In Europe, countries with historically high inflation saw greater homeownership, with 50% of homeowners citing inflation protection as a key motive. Similarly, immigrants in the U.S. from high-inflation countries also showed higher homeownership rates, suggesting that past inflation experiences significantly influence housing decisions, even in new economic environments. This is particularly insightful because it shows that even after moving to a country with a totally different economic environment and housing market, the past experience of inflation is still entrenched in people’s minds.

“They’re in a different country now. And still, you see in their financial decision-making, that they put a lot of weight on their previous experiences. If they come, say, from Argentina, with lots of high inflation, they constantly try to protect their money. And so that’s a really good example for how these experiences really affect and rewire you, even if you know it’s not relevant,” says Malmendier.

The neuroscience of experiencing a financial downturn

What does seeing increasingly higher prices at the gas pump and supermarket do the human brain? Every time we have a new experience, the brain forms new neural connections or synapses. When we experience the same thing all over again, these connections are strengthened.

In neuroscience, this phenomenon is known as “synaptic tagging” and it is crucial to learning and memory formation. It explains how certain experiences, particularly significant or emotionally charged ones, leave a lasting imprint on our brains.

When a synapse is “tagged” following certain activities, it marks the spot for later protein synthesis, vital for forming long-lasting memories. The proteins synthesized at these tagged sites reinforce the synaptic connections, cementing the memory.

Another closely related phenomenon is long-term potentiation (LTP); a long-lasting enhancement in signal transmission between two neurons that results from their synchronous stimulation. This process is also thought to underlie learning and memory.

Both synaptic tagging and LTP explain why certain experiences, especially those that are emotionally charged or significant, like financial crises, have a long-lasting impact on behavior.

These phenomena are tied together by the overarching theme of neuroplasticity, a key concept in neuroscience that refers to the brain’s ability to reorganize itself by forming new neural connections, reorganizing brain pathways, and even forming new neurons throughout life.

In this context, neuroplasticity simply teaches us that individuals’ financial behaviors and attitudes are never static but are shaped and reshaped by their experiences. For instance, experiencing a financial crisis can lead to the formation of new neural pathways associated with risk aversion or cautious investing.

In a 2021 study published in Review of Finance, Malmendier showed that “Depression Babies” (people who grew up during the Great Depression when the stock market crashed catastrophically) displayed a significantly lower rate of stock market participation compared to later generations.

The traumatic financial experience of the Great Depression would have created strong synaptic connections, making these memories more influential and persistent in decision-making. In this case, losing a lot of money at the stock market makes people weary to invest in the future, just like living through inflation can make people very protective of their money.

The researchers also found that these effects are mediated by a recency bias. Recent experiences have a stronger influence on individuals’ expectations and risk-taking behaviors compared to earlier life experiences.

Financial crises, market booms, or downturns — these aren’t just fleeting news items. The bottom line is that these significant financial dramas etch themselves into our brains, creating strong, tagged synaptic connections that influence our future financial behavior.

Experience effects are observed even among highly educated and specialized professionals, including professional decision-makers and experts in their fields. This even includes bankers, who should know better. For instance, Henry (Heinrich) Wallich was born in the early 1900s in Berlin in a family of bankers.

As a teenager, Wallich lived through the Weimar Republic’s infamous hyperinflation before immigrating to the United States, where he followed in his parents’ footsteps and achieved a successful career in the financial industry. Wallich ultimately served as one of the governors of the Federal Reserve Board from 1974 to 1986, a position in which he served with dignity.

However, the most notable thing about Wallich’s tenure is the fact that to this day he holds the record for the most dissents (27) in the Fed’s board meetings. Wallich would almost always object to monetary policy adjustments, warning that inflation was around the corner — even when it wasn’t a real concern.

Wallich just couldn’t shake off the specter of inflation, which he experienced in a different country overseas decades earlier, even though he was a Fed governor. Why? Because his experience of financial trauma made him act irrationally at certain times.

Similarly, people who experience betrayal or abuse might develop deep-seated trust issues. Someone who underwent traumatic experiences that involved physical danger, such as being mugged or fighting in war, can develop a heightened startle response and hypervigilance. We know from psychiatry that traumatic events can have long-lasting effects on people, so it’s quite fascinating that our economic models are only beginning to catch up with the science.

“A veteran who lives in Germany or the US might hear a loud noise, say of a car starting. To them, it sounds like a bomb coming down. You know there’s no danger, yet you have this immediate reaction as if that traumatic event was happening again.”

“This kind of rewiring happens also with economic trauma and events like the Weimar hyperinflation, but also the Great Depression in the US or the pandemic. These are all traumatic events, and we have to take this evidence, this neuropsychiatry evidence, seriously,” says Malmendier.

How long and how severely we experience a certain financial downturn, such as high inflation, matters a lot. The longer time gas pump prices keep increasing, the greater the risk that the inflationary event becomes etched in people’s brains, says Malmendier. Once the experience becomes long-lasting, there may be severe consequences for the economy.

Making sense of all this

This fresh neuroscience perspective on behavioral economics urges a rethinking of economic models and monetary policy. It suggests that to truly understand financial decision-making, we must consider the emotional and experiential components, not just the rational or informational aspects. Policymakers, in particular, should take heed of these realities. But what can they do?

Malmendier, who often advises German decision-makers and bankers in the European Central Bank, says it all starts with awareness. Recent global events, like the COVID-19 pandemic and the energy crisis, have left people more cautious and increasingly worried about price hikes, health issues, and an unstable professional landscape. This new mindset, Malmendier argues, must be a critical consideration in policy formulation.

“This whole concept of Gen X, Gen Y, Gen Z, Millennials, why is it? Why do we think generations, people born around the same time, behave similarly in certain ways? Well, they have common experiences that have shaped them. And that’s what policymakers need to take into account,” Malmendier says.

A key challenge for policymakers is addressing the ‘scarring’ left by such events. Many people become overly conservative in their economic decisions post-crisis, such as saving excessively rather than investing in themselves. To counter this, Malmendier suggests policies that tangibly demonstrate a return to normalcy, thereby helping to rewire people’s economic behavior.

Financial policy changes, like those concerning inflation control, are essential, but they must be complemented by visible changes in people’s day-to-day lives. The real litmus test for any policy is its tangible impact on the ground – at the supermarket, the gas pump, and in the wallets of individuals. People’s perception of the economy can sometimes generate a self-fulfilling prophecy.

When immediate changes in lived experience are not feasible, media and communication can play important roles. Malmendier suggests moving away from dry monetary policy announcements to more relatable, experiential forms of communication. The Central Bank of Jamaica, for instance, uses reggae songs to explain inflation; a creative approach to making economic concepts more accessible and engaging.

While crises leave long-lasting effects, these are not set in stone. Neuroplasticity means that our brain pathways — and thereby our behavior — always change with experience. It’s a two-way street. So positive and stable economic conditions over time can help rewire people’s attitudes and behaviors, gradually diminishing the impact of past traumas.

“The concept of neuroplasticity says that inflation scarring has long-lasting effects, but it also says that when the times are good again for long enough, you rewire again and things will get better,” Malmendier says.

[no_toc]